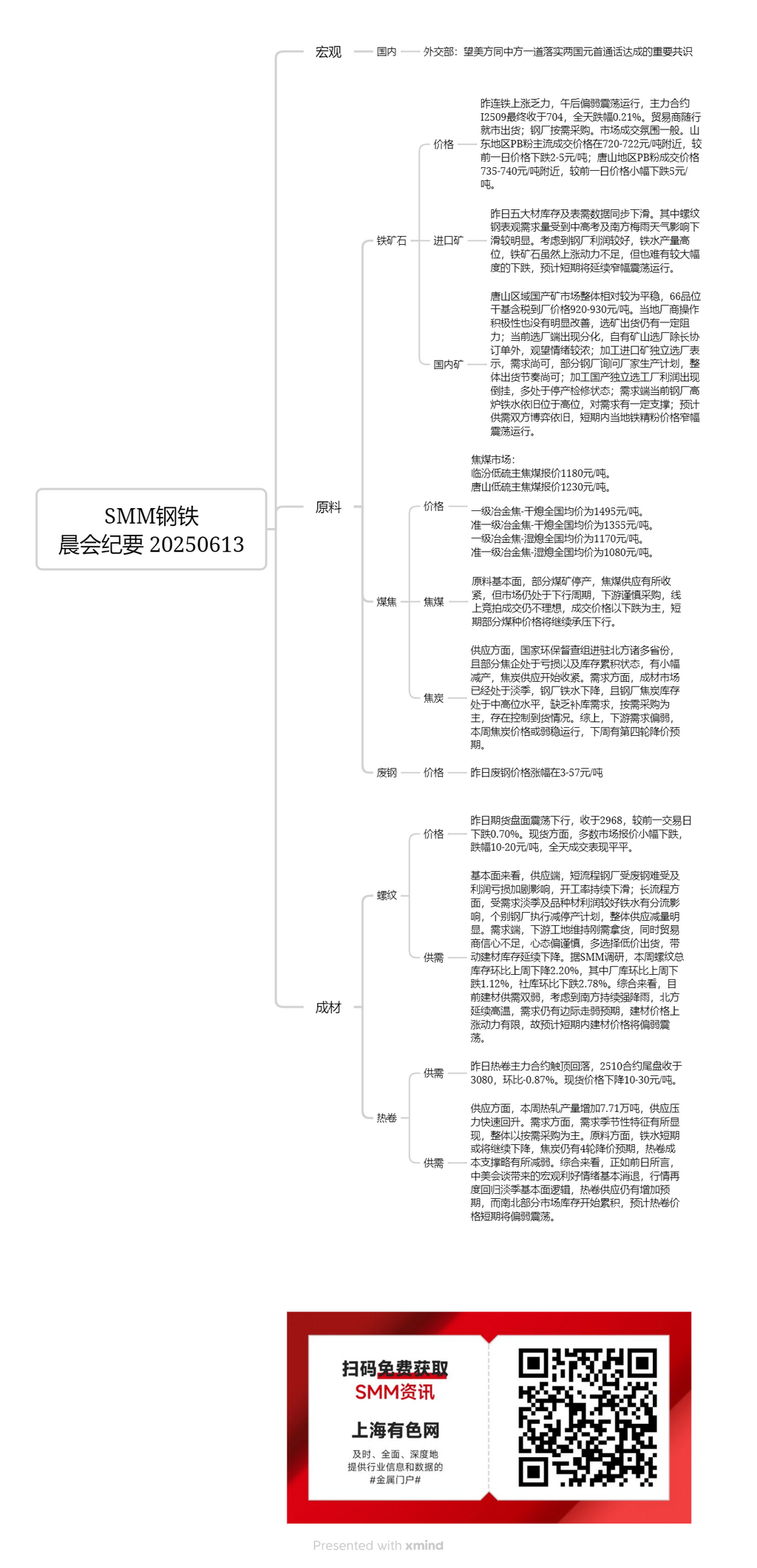

Domestic ore:

The domestic ore market in the Tangshan region remained relatively stable overall, with the 920-930 yuan/mt delivery-to-factory price (tax included) for dry-basis ore with a 66% grade. The operational enthusiasm of local producers did not improve significantly, and there was still some resistance in ore processing and shipments. Currently, beneficiation plants are showing signs of divergence. Beneficiation plants with captive mines, excluding those with long-term agreements, are exhibiting a strong wait-and-see sentiment. Independent beneficiation plants processing imported ore reported moderate demand, with some steel mills inquiring about production plans, and overall shipment pace remaining moderate. However, independent beneficiation plants processing domestic ore are experiencing inverted profits and are mostly in a state of shutdown for maintenance. On the demand side, pig iron production at steel mill blast furnaces remains high, providing some support to demand. It is expected that the tug-of-war between sellers and buyers will persist, and iron ore concentrate prices in the region will fluctuate rangebound in the short term.

Imported ore:

Yesterday, the DCE iron ore futures struggled to rise and traded in the doldrums in the afternoon. The most-traded I2509 contract eventually closed at 704, down 0.21% for the day. Traders sold according to market conditions, while steel mills purchased as needed. The market trading atmosphere was average. In the Shandong region, the mainstream transaction prices for PB fines were around 720-722 yuan/mt, down 2-5 yuan/mt from the previous day. In the Tangshan region, the transaction prices for PB fines were around 735-740 yuan/mt, down slightly by 5 yuan/mt from the previous day.

Yesterday, the inventory and apparent demand data for the five major steel products declined simultaneously. Among them, the apparent demand for rebar was significantly affected by the senior high school entrance examination, college entrance examination, and plum rain season in south China, leading to a notable decline. Considering the favorable profits of steel mills and the high level of pig iron production, although iron ore lacks upward momentum, it is also unlikely to experience a significant decline. It is expected that iron ore prices will continue to fluctuate rangebound in the short term.

Coking coal:

The quoted price for low-sulphur coking coal in Linfen is 1,180 yuan/mt. The quoted price for low-sulphur coking coal in Tangshan is 1,230 yuan/mt.

On the raw material fundamentals side, some coal mines have suspended production, leading to a tightening of coking coal supply. However, the market is still in a downward cycle, with downstream buyers exercising caution in procurement. Online auction transactions remain unsatisfactory, with transaction prices mainly declining. In the short term, prices for some coal types will continue to be under pressure.

Coke:

The nationwide average price for premium metallurgical coke (dry quenching) is 1,495 yuan/mt. The nationwide average price for high-grade metallurgical coke (dry quenching) is 1,355 yuan/mt. The nationwide average price for premium metallurgical coke (wet quenching) is 1,170 yuan/mt. The nationwide average price for high-grade metallurgical coke (wet quenching) is 1,080 yuan/mt.

In terms of supply, national environmental protection inspection teams have been stationed in many northern provinces, and some coking plants are experiencing losses and inventory accumulation, leading to slight production cuts and a tightening of coke supply. On the demand side, the finished steel market has entered the off-season, with a decline in pig iron production at steel mills. Additionally, steel mills' coke inventories are at a moderate to high level, lacking restocking demand. Purchases are mainly made as needed, with some control over arrivals. In summary, downstream demand remains weak. This week, coke prices are expected to remain in the doldrums, with a fourth round of price cuts anticipated next week.

Rebar:

Yesterday, the futures market fluctuated downward, closing at 2968, down 0.70% from the previous trading day. On the spot front, most market quotations dropped slightly, with declines of 10-20 yuan/mt, and overall trading performance was mediocre.

From a fundamental perspective, in terms of supply, EAF steel mills have been affected by difficulties in obtaining steel scrap and worsening profit losses, leading to a continuous decline in operating rates. For integrated steel mills, influenced by the off-season demand and the diversion of pig iron due to better profits from certain steel products, individual steel mills have implemented production reduction or suspension plans, resulting in a significant overall supply reduction. On the demand side, downstream construction sites continue to purchase based on immediate needs. Meanwhile, traders lack confidence and maintain a cautious mindset, preferring to sell at lower prices, driving a continued decline in construction material inventory. According to the SMM survey, this week's total rebar inventory decreased by 2.20% WoW, with in-plant inventory falling by 1.12% WoW and social inventory dropping by 2.78% WoW. Overall, the current supply and demand for construction materials are both weak. Considering the persistent heavy rainfall in the south and the prolonged high temperatures in the north, there is still an expectation of marginal demand weakening. The upward momentum for construction material prices is limited, so it is expected that construction material prices will remain in the doldrums in the short term.

HRC

Yesterday, the most-traded HRC futures contract peaked and then pulled back, with the 2510 contract closing at 3080, down 0.87% WoW. Spot prices fell by 10-30 yuan/mt. In terms of supply, HRC production increased by 77,100 mt this week, and supply pressure rebounded rapidly. On the demand side, seasonal characteristics of demand have emerged, with overall purchasing mainly based on needs. In terms of raw materials, pig iron may continue to decline in the short term, and there are still expectations for four rounds of coke price cuts. The cost support for HRC has slightly weakened. Overall, as mentioned the day before yesterday, the favourable macro sentiment brought about by the China-US talks has largely dissipated, and the market has once again returned to the fundamental logic of the off-season. There are still expectations for an increase in HRC supply, while inventory has begun to accumulate in some markets in the north and south. It is expected that HRC prices will remain in the doldrums in the short term.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)